The life insurance application process is often perceived as complicated, time-consuming, and intrusive. In an attempt to save money and attract customers who might be put off by the idea of mandatory medical exams or tests, many life insurance companies in the US have in recent years turned to accelerated underwriting (AU). This option has proved popular, as LIMRA reports that “More than half of consumers indicate they would be more interested in purchasing life insurance that was issued using accelerated underwriting.”

However, the opportunities of AU come with risks and challenges. Forgoing medical exams means the information that the provider can gather about the potential policyholder is now limited to what the applicant self-reports on their application, which may sometimes be incomplete or incorrect.

This potential misrepresentation threatens the legitimacy of AU in life insurance. To address this issue, SCOR’s Behavioral Modelling team, in partnership with the SOA, investigated the possibility of using concepts from behavioral science to redesign a life insurance application form and increase disclosure rates.

Experiment Design

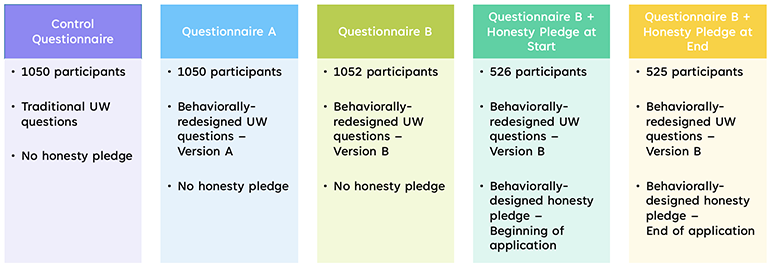

The researchers conducted an online experiment involving over 4,000 participants. These participants were divided into five groups and presented with either a standard sample life insurance application or one that had been redesigned based on ideas from behavioral science. After participants completed the forms, the team compared disclosures between the groups to determine the effect of the redesign. (See Figure 1)

Figure 1

Experiment Groups

Behavioral Science Concepts

Behavioral science is the study of human decision-making and focuses on understanding how our decisions are influenced by psychological and environmental factors. Several of these factors went into the redesign of the application forms in the experiment.

Cognitive Load

For instance, one important concept in behavioral science is cognitive load. This is the amount of mental effort required to complete a task. Humans only have a certain amount of cognitive bandwidth available at any given time, so if a task is too frustrating or overwhelming, we can experience cognitive overload. When this happens, we will often look for shortcuts or abandon the task entirely.

Insurance applications can be complicated, confusing forms, requiring large amounts of brainpower to get through. An applicant can easily be overloaded, and they will then resort to putting down whatever answers are easiest. This can obviously lead to misrepresentation, as the applicant rushes through the form and fails to think through their answers carefully.

SCOR’s experiment explored how to make it easier for an applicant to complete the process so they can give more considered responses.

Social Norms

Another concept of note in behavioral science is that of social norms. Humans are social creatures—we like the feeling of being part of a group and will often change our behavior to conform. This means that when we are challenged to admit to a behavior that is socially stigmatized, we will often bend the truth or find ways to justify to ourselves why we don’t need to answer honestly. This is a way to protect ourselves from the negative feelings that come from violating the all-important social norms of our community.

In the context of insurance, where we often ask about sensitive topics, it’s important to be aware of the social norms surrounding the questions we write. SCOR’s experiment investigated ways to use this understanding of social pressure to encourage honest disclosure, rather than hindering it.

Mental Health Conditions

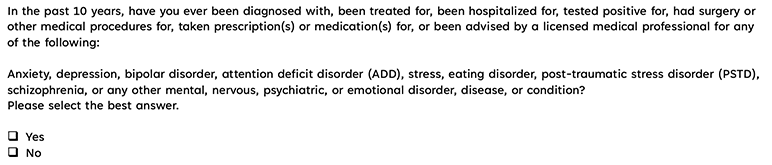

The experimental redesign applied both of these concepts—cognitive load and social norms—to several different questions that are typically included on a life insurance application form. For instance, in the past, applications might have traditionally asked about mental health conditions as shown in Figure 2.

Figure 2

Control Mental Health Question

As you can see, this format asks about all mental health conditions in one long list, with one Yes/No response. If you’ve had any of the listed conditions, you are supposed to check the box “Yes” to all of them.

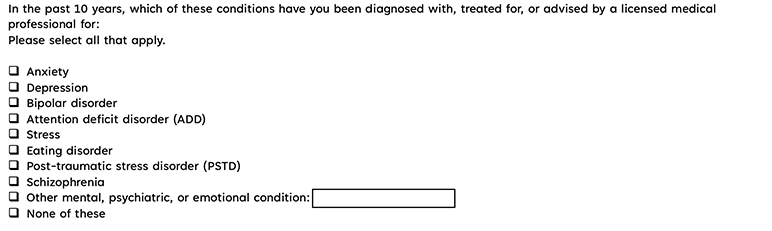

As show in Figure 3, this question was redesigned to incorporate ideas of cognitive load and social norms.

Figure 3

Redesigned Mental Health Question (Questionnaire A)

Cognitive Load

Due to the cognitive load required to get through a life insurance application, many applicants may quickly become tired, frustrated, and anxious to get through the process quickly. This can lead to skimming, where the applicant fails to carefully read the entire text of a question and instead just scans through it.

When a reader is skimming, large blocks of text are much harder to scan quickly and are therefore much more likely to be skipped with barely a glance. The applicant may read the title “Mental Health Conditions,” and think, “Well, I’ve had depression in the past, but that’s not really important enough to bother reporting,” and simply check “No” before moving on.

The bullet point lists in the redesigned version are much easier to read quickly. Each mental health condition stands on its own and doesn’t get lost among the others. It’s much more likely that the applicant will notice their condition and report it.

Social Norms

This question also applies the idea of social norms. Mental health remains an often-stigmatized subject, especially when it comes to certain mental health topics.

In the Control version of the question, someone who has depression, for instance, must check the same box as anyone with schizophrenia or bipolar disorder. But these conditions often carry much greater levels of social stigma than more socially accepted conditions like depression or anxiety.

This means that an applicant with depression may hesitate to be included in the same category as all the other conditions. They may instead find ways to justify to themselves why the question doesn’t really apply to them, since it is asking about more severe conditions.

In the redesigned version of the question, we eliminate that concern by allowing participants to check only the conditions that apply to them. So, a participant with depression only needs to check the box for depression. This could help alleviate concerns about social stigma and allow participants to feel more comfortable being honest.

Results

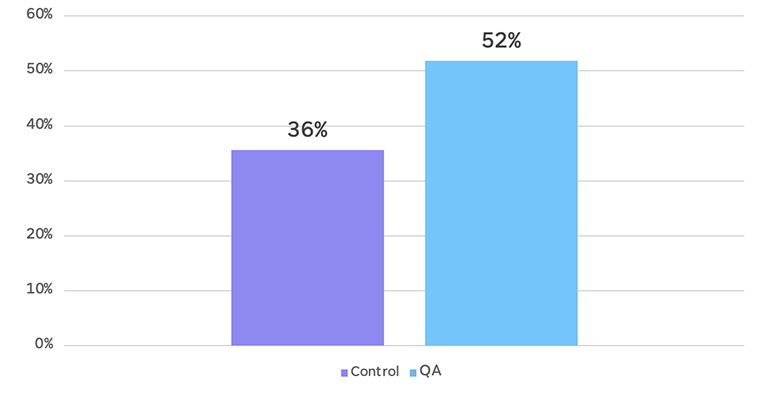

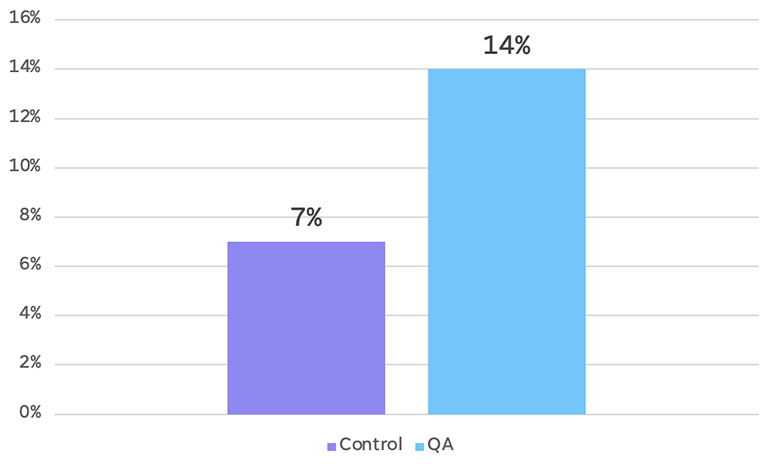

After the experiment, the researchers compared the mental health disclosures from participants that saw the Control version of the form and those that saw the redesigned version. Around 36% of participants in the Control group disclosed any mental health condition, while this percentage was around 52% in the redesign group. This represents a 46% increase in mental health disclosures from this small change in wording. (See Figure 4)

Figure 4

Mental Health Question Results

Percentage Disclosing Any Mental Health Condition

Further, most of the increase in the redesign group was due to higher rates of disclosure of conditions such as stress, depression and anxiety. This supports the hypothesis that the redesign helped participants with relatively socially-accepted conditions to feel comfortable disclosing, since they no longer had to lump themselves in with all of the other conditions listed.

By harnessing the concepts of cognitive load and social norms, the redesigned question was able to encourage more honest disclosure on this sensitive topic.

Medical Conditions

As with mental health conditions, other medical conditions are often grouped in long lists. These are often organized by body system, with one Yes/No response required for each group of conditions. This is how the Control questions on medical conditions were presented in the experiment.

The redesigned version of this question maintained that format but added an extra element. If a participant did not report diabetes, cancer or heart disease in the initial list of conditions, then after the end of the medical conditions questions, they were asked to confirm they had not had the conditions they hadn’t reported. (See Figure 5)

Figure 5

Redesigned Medical Conditions Confirmation Question (Questionnaire B)

Cognitive Load

As mentioned above, long lists of multiple conditions can easily lead to cognitive overload. This can quickly cause skimming—overwhelmed by all the information, the applicant may begin reflexively answering “No” to each list, without reading them carefully to confirm that their conditions are not listed.

The confirmation question highlights three of the most important, common conditions and gives participants a second chance to report them. If they have missed these conditions in their reading of the previous lists, they are much more likely to notice them now. This also breaks the pattern of the previous questions and therefore gives participants a reason to pause in their skimming and pay attention.

Results

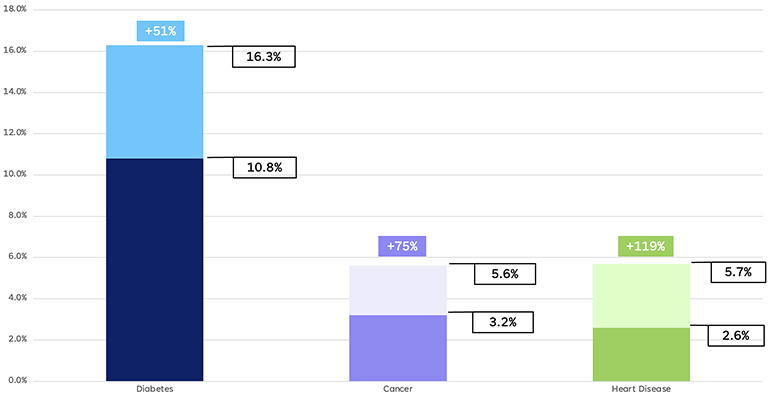

In Figure 6 below, the darker, lower portion of each bar represents the percentage of participants who disclosed that condition in the initial set of questions, while the lighter, upper bar represents the total disclosure after the confirmation question. For all three conditions, the confirmation question produced 50–120% increases in disclosure. For heart disease in particular, more participants disclosed in the confirmation question than did in the initial list of questions.

Figure 6

Confirmation Question Results

Percentage Disclosing Medical Conditions

These results show that the confirmation question did serve to prompt extra disclosure. Many participants who apparently missed a condition they should have reported the first time around took advantage of the second chance offered to slow down and pay attention. This ultimately led to increased disclosure.

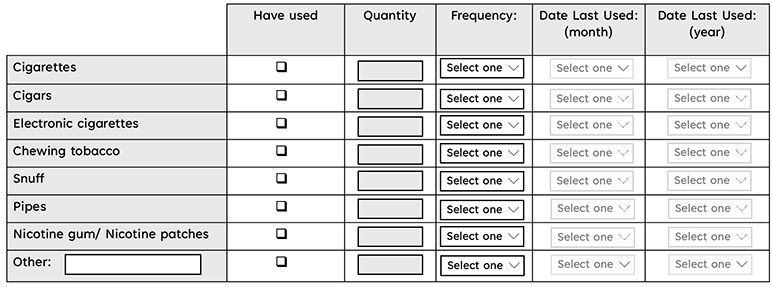

Tobacco Use

Another area of potential nondisclosure is in questions around lifestyle factors, such as tobacco usage. Unfortunately, one common way of asking about this issue, as shown in the Control version of this question, is not very helpful. (See Figure 7)

Figure 7

Control Tobacco Use Question (Parts 1 & 2)

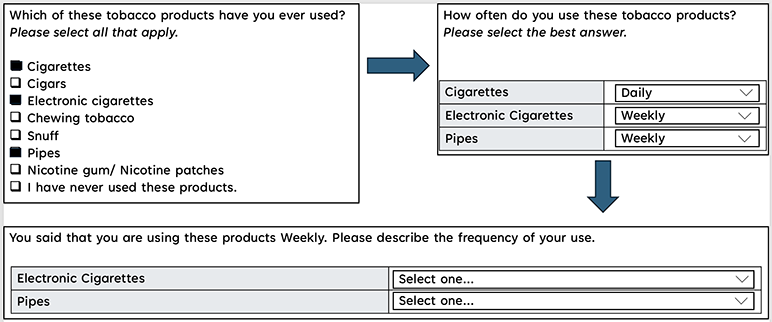

The question was redesigned as shown in Figure 8 below:

Figure 8

Redesigned Tobacco Use Question (Questionnaire A)

This redesign splits the question into multiple pages, with the participant’s answers on one page influencing what they see on the next.

Cognitive Load

The Control version of this question, especially Part 2, is overwhelming and intimidating even at first glance. Again, this is likely to produce feelings of cognitive overload and provoke behaviors like skimming. This may lead to an applicant simply trying to fill in the answers that let them progress past the question as quickly as possible, regardless of the truth.

The redesigned version of the question takes this into account and aims to reduce feelings of cognitive load by separating the questions into sequential pages with a clear flow between them. This means that the participant never confronts too much information at once and therefore is not likely to be overwhelmed. They are also able to progress logically through the process and provide information in steps, encouraging them to slow down instead of skimming.

Social Norms

Tobacco use is another subject that carries various social stigmas. The Control version of this question doesn’t explicitly state a social norm in Part 1—tobacco use is presented completely neutrally, in a simple Yes/No format.

But no behavior is actually ever viewed as neutral. It is likely the participant will know that society generally views tobacco use negatively and that insurance companies are even more likely to do so. This means a participant may assume that the desired, acceptable behavior here is to not use tobacco and may therefore answer “No.”

Another issue, as with the Mental Health question, is that Part 1 of the Control question groups all types of tobacco products together. Again, humans are very sensitive to social stigmas, and different products carry different stigmas. Electronic cigarettes in particular are often viewed in a different light than other products. This means that if a participant only uses e-cigarettes, for instance, they may think, “Well, that’s not really the same thing as ‘tobacco use.’ That’s not really what this question is about.”

In the redesigned version of this question, the social norm is supplied for the participant. By framing the question to assume that the participant does use tobacco and skipping directly to asking which kinds of products they use, tobacco use is framed as the default, expected, normal behavior.

In addition, the redesigned question separates types of tobacco products and allows the participant to only admit to those that they use. As with the Mental Health question, this could help put participants at ease and encourage them to honestly disclose their use.

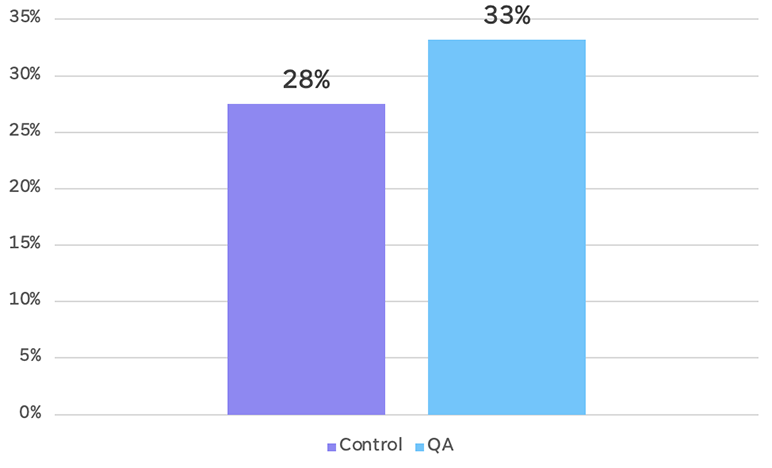

Results

The redesigned version of the Tobacco Use question produced a 21% increase in disclosures of current tobacco use. It appears that the cleaner, less cognitively-taxing design and the reassuring framing helped encourage disclosure. (See Figure 9)

Figure 9

Tobacco Use Results (Overall)

Percentage of Current Tobacco Users

As with the Mental Health results, part of this increase in disclosure was due to an increase in disclosures of relatively socially-accepted forms of tobacco use. For instance, electronic cigarettes saw a 100% increase in disclosure in the redesigned format. The change in formatting allows participants that only use electronic cigarettes to differentiate themselves from other tobacco users, encouraging disclosure. (See Figure 10)

Figure 10

Tobacco Use Results (Electronic Cigarettes)

Percentage of Current E-Cigarette Users

Conclusion

These results highlight just three of the areas explored in this experiment and just two of the behavioral science principles applied to the design of life insurance applications. Other questions covered include Height/Weight, Weight Change, Alcohol Use, and Substance Use Support. Overall, the experiment showed that behavioral science concepts can help make the process easier for applicants and promote more honest disclosure. This means a valid contract for both parties, ensuring no complications at the claims stage for either the policyholder or the insurance company.

To read more about the results of this experiment and its implications for application design, access the full study report and interactive dashboard here.

This article is provided for informational and educational purposes only. Neither the Society of Actuaries nor the respective authors’ employers make any endorsement, representation or guarantee with regard to any content, and disclaim any liability in connection with the use or misuse of any information provided herein. This article should not be construed as professional or financial advice. Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Caitlyn Parsons is a behavioral science analyst with SCOR. She can be reached at cparsons@scor.com.

Carolyn Covington is a VP, marketing actuary with SCOR. She can be reached at ccovington@scor.com.