The 2024 LIMRA Barometer[1], a study of Americans’ perceptions, knowledge and behavior regarding life insurance, estimated 75 million in the U.S. need life insurance and 25 million need more than what they currently have. These findings represent an insightful opportunity for life insurers to consider. However, life insurance can be confusing to many people. In fact, the 2024 LIMRA Barometer also found that 41% of respondents stated they were only somewhat or not at all knowledgeable about life insurance. When the public doesn’t understand how it works or what it offers, they’re less likely to buy it.

Behavioral science offers life insurers some tools that may help overcome this challenge. This behavioral perspective provides practical communication techniques that life insurers may consider applying to their marketing to help people better understand their products.

Assisting System 1 Thinking

The first step to improve comprehensibility of life insurance products is understanding how potential customers process information. While human beings’ attention span, memory, judgement and decision-making have definite limitations, we successfully juggle many tasks at once in our daily lives. This is because humans have the ability to apply fast, automatic, even unconscious thought processing, which psychologists call System 1 thinking. Immediately recognizing a brand logo on a package, or reading a “beach” novel, or driving a car: These are all examples of System 1 thinking.

The Society of Actuaries (SOA) Research Institute and RGA conducted a study[2] in 2024 to uncover whether behavioral science techniques applied to a fictional life insurance website improved consumer comprehension. Researchers found that techniques that highlighted important information about life insurance products assisted System 1 thinking and boosted comprehension by 21%. Some of these techniques included summaries, offering “frequently asked questions” and using simple icons to highlight pertinent information.

Engaging System 2 Thinking

To complete complex tasks, like calculating numbers, learning something new, or making complicated decisions, people need to engage in a more deliberative and logical effort, which behavioral scientists refer to as System 2 thinking.

Customer journeys typically focus on streamlining the sales process by making information brief. But sometimes it’s effective to encourage deep engagement, in other words, System 2 thinking. Techniques that disrupt the automatic interactions of System 1 thinking and, instead, prompt reflection often employ a concept known as “positive friction.”

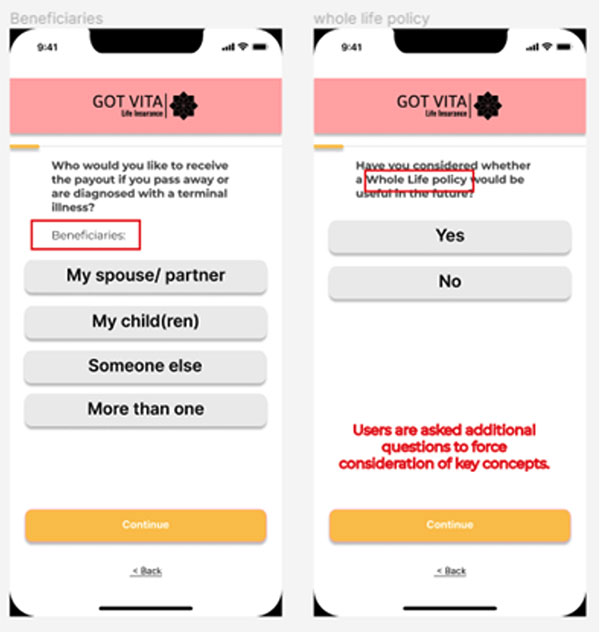

One example of positive friction is to prompt customers to answer questions, which encourages consideration of key concepts (see Figure 1). Making sure information is relevant to customers’ experiences by personalizing it is another type of positive friction technique. An online tool, such as a sliding scale or calculator, gives people control over how they interact with information, helps clarify information and customizes the customer journey.

Figure 1

Fictional Life Insurance Website, Using Positive Friction Techniques[3]

The SOA Research Institute/RGA experiment applied System 1 best practices (e.g., simple language, important information at the top of the page) to a fictional website while also creating positive friction to encourage deeper thinking. The positive friction techniques included questions prompting participants to list beneficiaries and a calculator that assessed their insurance needs. These techniques improved overall comprehension by 28%. Additionally, participants who viewed this screen scored 59% higher than those in the control group on questions about concepts and terminology.

Reaching the TikTok Generation

In 2023 the SOA Research Institute surveyed 1,000 U.S. consumers, aged 21 through 42, about how they understood, investigated and purchased insurance. Results were published in “Perceptions of Younger Generations on Risk and Insurance.”[4] One finding revealed that 23% of respondents indicated they intended to buy life insurance within the coming year.

With a quarter of this age group planning on shopping for life insurance, it’s important to remember the popularity of video with younger consumers. Social media app TikTok reached an estimated 1.6 billion users in 2024, according to Business of Apps[5], and 66% of them were between the ages of 18 and 44. It’s obvious we live in a video age. In addition to being an increasingly popular medium, it also may be effective in sharing information.

Experimenting with Video and AI Avatars

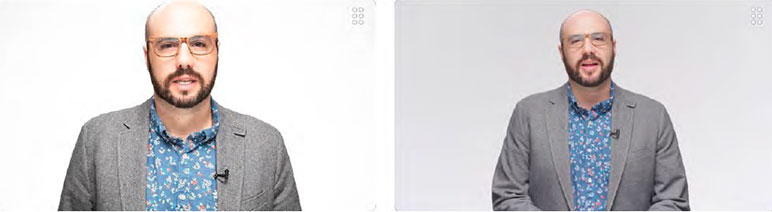

In an additional experiment with behavioral science techniques, the SOA Research Institute and RGA tested the effectiveness of video in sharing information about life insurance with consumers. Researchers recruited 2,005 U.S. participants and measured their comprehension of information that had been presented in various formats on a website: Text, a video featuring an actor, and a video featuring an artificial intelligence (AI)-generated avatar based on the actor’s appearance.

The experiment’s video featured a presenter who spoke with a North American accent and appeared in a blue shirt, suit jacket, and glasses. The script followed the website’s text exactly, ensuring consistency across formats.

Left: AI-generated video avatar; Right: Human actor in video

To create the AI avatar, researchers used a headshot of the human presenter, captured during filming. Specialized software then animated this image, enabling the AI avatar to deliver the identical script. Different versions of the website were presented to participants, one with a video featuring the human presenter and the other with an AI-generated messenger. Both videos were placed at the beginning of the website’s information section, providing users with a clear introduction.

Results: Overall Comprehension

First, the experiment compared comprehension between websites with and without video. Results found that the addition of video to a website that also used methods to encourage both System 1 and System 2 thinking increased comprehension by 15%. However, adding video to a website that only encouraged System 1 thinking showed little impact.

In the experimental context, participant perception of the messenger as credible, expert and having a similar cultural background significantly increased user comprehension.[6] On the other hand, if the presenter was perceived as unsettling, even if likable, comprehension decreased. Because the AI avatar was viewed as more unsettling than the human presenter, the video with the actor resulted in slightly higher comprehension. However, the difference between the human and the avatar was small enough that the cost savings of the avatar might make it worth consideration.

More Options for Personalizing the Customer Journey

Other AI tools, such as digital assistants, could be helpful to make information personally relevant and encourage deeper consideration by answering potential customers’ specific questions, as discussed in the SOA Research Institute report, “The Insurance Market in the Era of Digital Transitions.”[7] Also, life insurers might be able to leverage generative AI to employ System 2 thinking techniques by designing personalized life insurance products based on a customer’s risk profile and coverage needs.

Dive Deeper

For more details about behavioral science techniques that help explain life insurance products to consumers and to learn more findings from comprehension experiments, download the SOA Research Institute report, “Searching for Simplicity: Using Behavioral Science to Make Life Insurance Product Information Simple and Effective.”

This article is provided for informational and educational purposes only. Neither the Society of Actuaries nor the respective authors’ employers make any endorsement, representation or guarantee with regard to any content, and disclaim any liability in connection with the use or misuse of any information provided herein. This article should not be construed as professional or financial advice. Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Dale Hall, FSA, MAAA, CERA, is managing director of research for the SOA Research Institute. Dale can be contacted at dhall@soa.org.

Endnotes

[1]Stephen Wood, Maggie Leyes. “2024 Insurance Barometer Study,” LIMRA, 7/15/2024, https://www.limra.com/en/research/research-abstracts-public/2024/2024-insurance-barometer-study/

[2] Rosmery Cruz, Peter Hovard, Shilei Chen and Matthew Battersby. “Searching for Simplicity: Using Behavioral Science to make Life Insurance Product Information Simple and Effective,” Society of Actuaries, August 2024, https://www.soa.org/resources/research-reports/2024/behavioral-science-rga/?utm_source=community+news+letter&utm_medium=article&utm_campaign=Behavioral+Science+article&utm_id=Behavioral+Science+article

[4] Eric Sondergeld, Marie Ammar and Greenwald Research. “Perceptions of Younger Generations on Risk and Insurance,” Society of Actuaries, April 2023, https://www.soa.org/resources/research-reports/2023/young-gen-private-ins/?utm_source=community+news+letter&utm_medium=article&utm_campaign=Behavioral+Science+article&utm_id=Behavioral+Science+article

[5] David Curry, “TikTok Revenue and Usage Statistics (2026)” Business of Apps, Updated Jan. 7, 2026, https://www.businessofapps.com/data/tik-tok-statistics/

[7] Arthur Charpentier and Raphaël Suire. “The Insurance Market in the Era of Digital Transitions: Relationships Between Insurers, Big Tech, and Insurtechs,” Society of Actuaries, January 2025, https://www.soa.org/resources/research-reports/2025/big-tech-insurance/?utm_source=community+news+letter&utm_medium=article&utm_campaign=Behavioral+Science+article&utm_id=Behavioral+Science+article