Actuaries have been taught that a Market Value Adjustment (MVA) shifts risk to a contract owner. Presence of an MVA results in the insurer being able to credit a higher rate of interest as it passes interest rate risk to the contract owner. Traditional actuarial discussions often describe the advantages of including an MVA in a deferred annuity product. During a normal interest rate cycle with moderate interest rate movements, it works perfectly well. When the reference rate experiences larger decreases, the MVA can become a potential liquidity risk for the insurer. The insurer might owe an amount far more than the Accumulation Value in this situation across a wide swath of the deferred annuities with MVAs in force upon surrender.

Throughout this article, Accumulation Value refers to the contract value prior to surrender charges and MVA, while Cash Surrender Value reflects these adjustments.

If the MVA reference rate increases, the MVA causes an additional charge to the contract owner whenever enough is withdrawn for MVA to occur; typically, MVA is simultaneous with surrender charges. The MVA charge is limited by the Nonforfeiture Value; thus, if the MVA brings the amount down below the Nonforfeiture Value, then MVA must be partially or completely waived to bring the value up to at least the Nonforfeiture Value. The insurer cannot pay less than the Nonforfeiture Value upon a full surrender.

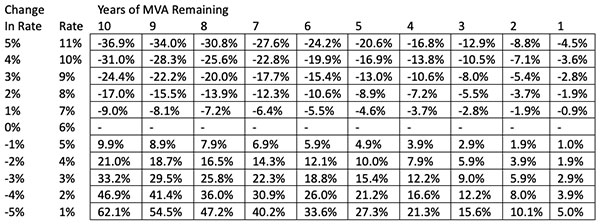

If the MVA reference rate decreases, the MVA causes an additional amount to be paid to the contract owner. It is this additional amount above the Accumulation Value that is a liquidity risk. This amount is theoretically only limited by how low the reference rate can go. The additional amount will be greater the lower the starting MVA reference rate, subject to the same decrease. Table 1 below illustrates the potential magnitude of an MVA credit, and is not intended to represent all product designs.

Table 1

MVA Credit% (- number is a Charge) Based on a Change in MVA Reference Rate

Starting MVA Reference Rate = 6.00% MVA Credit% = (1.06 / (1.06 + Change in Rate)) ^ Years of MVA Remaining – 1 Total Obligation = Accumulation Value * (1 + MVA Credit% – Surrender Charge%)

Example for seven years remaining and 300bps decrease: MVA Credit% = (1.06 / (1.06 - 0.03)) ^ 7 – 1 = 22.3% Total Obligation = Accumulation Value * ( 1 + 22.3% - Surrender Charge%) If nothing changes after a year, the MVA Credit% decreases from 22.3% to 18.8%.

The -100bps column appears to be like a surrender charge schedule, and these amounts would largely offset a contract’s surrender charge percentages. In the event of a 100bps drop an insurer might pay an amount close to the Accumulation Value upon a full surrender.

As the decrease becomes more severe, the amounts start exceeding the Accumulation Value by significant percentages. This is the source of the liquidity risk, as a large proportion of contracts may be in this situation at the same time, even if they are somewhat dispersed with varying years remaining in the MVA period and various starting MVA reference rates.

Exact formulas for an MVA vary between insurers and sometimes between various sets of contracts sold by an insurer. Check the exact formula used in any specific set of products to see the effect. The effect will be similar for any MVA formula in use.

Table 1 is a pricing view. To see the actual effect on an insurer as a valuation view, consider tracking where the MVA is currently on a block of business and perform a “what if” the reference rate instantaneously decreases 300bps. A 300bps instantaneous decrease is used here as an illustrative stress scenario commonly applied. An MVA tracker will show, in dollar terms, the amount above the Accumulation Value the insurer would have to pay upon surrender if the reference rate decreases 300 bps. This is an “all surrender” view. Of course, it is not realistic to think all the contract owners in this situation would surrender to collect the additional amount from the MVA.

Two concepts help create what may be a false sense of security. The first is that the interest crediting rate after a large decrease in MVA reference rate will be considerably lower than keeping the current contract; thus, surrender is unlikely. This view assumes competition is a deferred annuity of a similar type, which is increasingly not the case. There is a much larger world of competing savings/investing vehicles available compared to when MVA was first incorporated into deferred annuity products. It ignores the MVA credit, which may be substantial. The second is that, in the past, the MVA amount was not visible or easy to obtain for a particular contract. Now the MVA is increasingly visible on a real-time basis to agents and contract owners. In some cases, increased visibility of the MVA may create incentives for agents to now monitor for individual contracts where an amount higher than the Accumulation Value is available and then move the money to another contract for another full commission.

The contract owner might act while this temporary period—during which the amount available upon full surrender exceeds the Accumulation Value—persists. An advisor might now tell more contract owners to move their money and lock in that amount even if the new credited interest rate is lower.

While individual contracts may appear independent under stable conditions, large reference rate movements can introduce correlation across the block. Independence starts disappearing when the decrease in reference rate occurs, especially for sharper and larger decreases. For an insurer, the effect may resemble a wave. For reinsurers, the combined effect across multiple assumed blocks could be significantly larger than for a single direct writer, highlighting the potential significance of MVA provisions in deferred annuity contracts.

In practice, the MVA charge is typically constrained by the Nonforfeiture Value, while the MVA credit may be less constrained, creating an asymmetry in outcomes. Insurers use two main methods to implement an MVA limit and mitigate the liquidity risk. The Interstate Compact standards allow an MVA limit to be filed; however, the limit must be calculable as a dollar limit. Some companies have implemented an MVA limit and have fully or partially treated this risk.

One common method is to limit the MVA to the remaining surrender charge. The MVA is defined normally in policy forms, and then a single sentence is added that says the MVA, positive or negative, is limited to the remaining surrender charge. If the surrender charge is 6% at a point in the contract’s life, then the MVA charge is at most that same surrender charge dollar amount, limited by Nonforfeiture Value, and the MVA credit is at most that same surrender charge dollar amount. The insurer never pays more than the Accumulation Value as the boundary condition (the MVA credit with this limit completely offsets the remaining surrender charge). It is easy for an agent or customer service to explain whenever a question is asked. This method eliminates the liquidity risk.

A second, less common method is to limit the MVA credit to a mirror of the MVA charge limit. The maximum MVA charge or credit is set equal to the quantity {Cash Surrender Value prior to considering MVA – Nonforfeiture Value}. This is difficult to describe in policy forms, difficult for agents and customer service to explain whenever a question is asked, and the maximum exceeds the Accumulation Value, though not by nearly as much as if the MVA is unconstrained. This method does not decrease the MVA limit as the contract ages; in fact, it increases as more MVA can be charged or credited in later years. This method will limit, though not eliminate, the liquidity risk.

Other MVA limits are possible, one approach being a percentage limit. In the past, variations of this approach were sometimes implemented. In this approach, limit the MVA charge to no more than X% of Accumulation Value and limit the MVA credit to that same dollar amount. A potential value for X might be somewhere near 5%. This approach may have fallen out of favor because it may not seem fair that the MVA limit doesn’t decrease as the contract ages. The maximum will exceed the Accumulation Value, though not by nearly as much as if the MVA is unconstrained. This method will limit, though not eliminate, the liquidity risk.

All the methods will limit the MVA to reduce the liquidity risk compared to an unconstrained MVA. Only the one method that limits the MVA to the remaining surrender charge fully eliminates the potential to ever pay more than the Accumulation Value.

In Asset Adequacy Testing (AAT) the actuary will change the MVA reference rate with the same change that applies to the interest rate yield curve. However, few AATs include an opportunistic lapse when more than the Accumulation Value is available upon a full surrender. This concept of “in-the-moneyness” for an MVA is not well recognized. As an illustration of how this risk might be explored, one possible sensitivity would assume an opportunistic lapse in which, for example, 20% of the contracts fully surrender when the amount available upon full surrender is more than the Accumulation Value. If the insurer has unconstrained MVA, the results may be eye-opening. If the entire block is limiting MVA to the remaining surrender charge, then this sensitivity would show no difference.

The MVA is sometimes waived. Upon annuitization, MVA and the surrender charge are frequently waived (though sometimes further conditions apply to waiving MVA for a certain period only annuitization). Upon death, MVA and surrender charges are almost always waived. This sets up a situation where, depending on the contract’s MVA situation, there might be more value immediately prior to death than upon death.

Also, upon death, the Accumulation Value may be paid even if the amount is less than the Nonforfeiture Value, depending on how the product is filed (see Standard Nonforfeiture Law for Individual Deferred Annuities, Section 9: Disclosure of Limited Death Benefits). With minimum guaranteed interest rates in current products well below the Nonforfeiture Interest Rate, it is increasingly possible that Accumulation Value might eventually be less than Nonforfeiture Value. In certain circumstances, the relative values payable immediately prior to death versus upon death may differ. This could be alleviated by comparing the death benefit to the Nonforfeiture Value and the greater value paid, even when the product has a limited death benefit.

MVA was invented and implemented decades ago. Insurers may benefit by taking another look at this contract provision and making sure it is still working as expected.

The views expressed here reflect the author’s perspective based on industry experience and are intended to highlight potential considerations rather than to prescribe practices. This article is provided for informational and educational purposes only. Neither the Society of Actuaries nor the respective authors’ employers make any endorsement, representation or guarantee with regard to any content, and disclaim any liability in connection with the use or misuse of any information provided herein. This article should not be construed as professional or financial advice. Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

John Blocher, FSA, MAAA, is the chief risk officer, vice president & actuary with Liberty Bankers Insurance Group. He can be reached at john.blocher@lbig.com.