Lower inflation during the last few decades, as demonstrated by lower bond yields, has made certain insurance products unattractive. Some insurance companies have either taken losses or discontinued products, and others have written down the values substantially as the products have been reprised under a lower interest rate regime. This article argues that higher US bond yields caused by higher inflation and substantially larger US deficits could make long-term care (LTC) insurance a viable offering again. This insurance covers the cost of long-term care services, such as nursing home care, home health care and assisted living. It is designed to help individuals pay for the high costs of long-term care, which can be very expensive and quickly deplete a person’s savings. Hedging that product will be easier as higher yields make the product tenable and the underlying profits attractive for insurance companies. This is a win-win situation in which market forces can match the issuer of debt (US federal government) and the buyer of that debt (LTC insurance policyholders) through a financial intermediary (insurance companies) that has a profitable business model.

Very long maturity bonds can be used to hedge the risk associated with LTC insurance. These bonds have a maturity of 30 years or more, and they are typically issued by governments or corporations. In the context of LTC insurance, very long maturity bonds can be used to hedge the risk of interest rate changes that may affect the cost of providing long-term care services over a substantial period of time. For example, if interest rates rise over the next 30 years, the cost of providing long-term care services may increase, which could result in higher premiums for LTC insurance policies. By investing in very long maturity bonds, insurance companies can lock in a fixed rate of return, which can help to mitigate the risk of interest rate fluctuations and thereby indirectly fund the growing federal budget deficit.

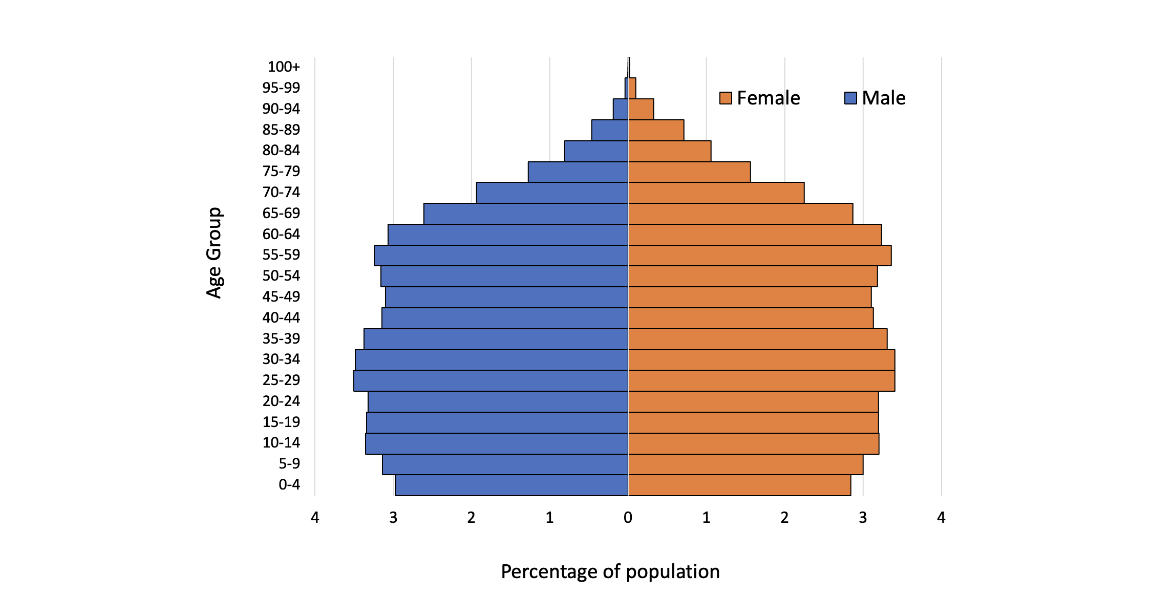

According to a report by Grand View Research,[1]the long-term care market in the United States was valued at $489.9 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 6.2% from 2024 to 2030. The market is driven by factors such as the aging population, the increasing prevalence of chronic diseases and rising health care costs. The US population pyramid in Figure 1 shows that a larger cohort of the population will need LTC insurance in the coming years. Life insurance companies can fill the void through the introduction of an LTC policy with added/embedded investments.

Figure 1

US Population Pyramid (2020)

The population pyramid gives a visual representation of a nation’s population structure, illustrating its distribution of age groups and genders. In the case of the United States, the population pyramid has undergone significant transformations over the years, influenced by factors such as birth rates, life expectancy, immigration and socioeconomic dynamics. Understanding the current state of the US population pyramid and predicting its evolution over the next 10 to 20 years is crucial for policymakers, economists and social scientists alike, as it sheds light on various socioeconomic challenges and opportunities associated with aging demographics.

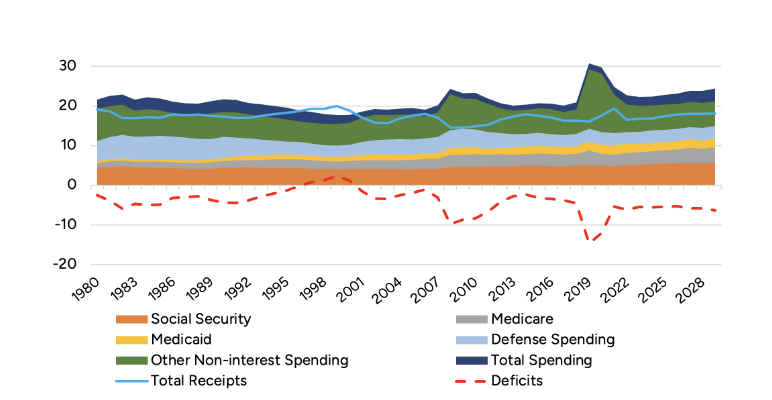

US Deficit Projections

In the Congressional Budget Office’s (CBO’s) projections, the deficit amounted to 5.3% of gross domestic product (GDP) in 2023 as shown in Figure 2. (Deficits and spending have been adjusted to exclude the effects of shifts that occur in the timing of certain payments when October 1 falls on a weekend.) Deficits fluctuated over the next four years, averaging 5.8% of GDP.[2] Starting in 2028, they are expected to grow steadily; the projected shortfall in 2033 is 6.9% of GDP—significantly higher than the 3.6% of GDP that deficits have averaged over the past 50 years.[3]

Figure 2

Spending vs Receipts History and Projections

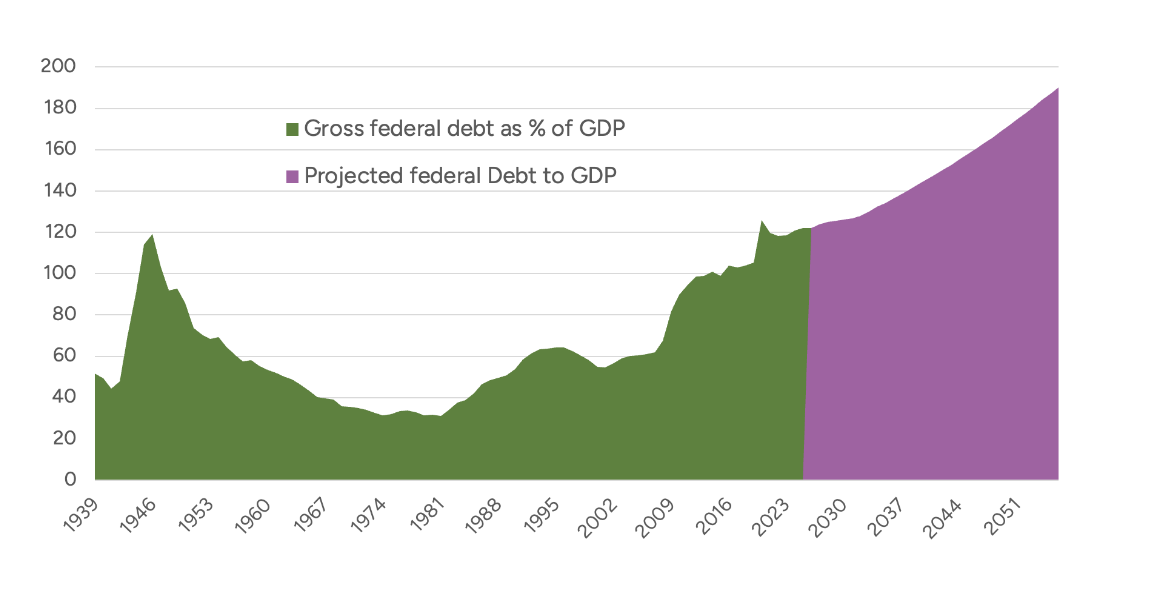

Federal debt held by the public is projected to increase in each year of the projection period and to reach 118% of GDP in 2033—higher than it has ever been. In the two decades that follow, growing deficits are projected to push gross federal debt higher still as shown in Figure 3, to 190% of GDP in 2056.[4]

Figure 3

Gross Federal Debt and CBO Projection

Source: Congressional Budget Office, “The Long-Term Budget Outlook: 2026 to 2056,” CBO, February 2026.

Current Market Size and Future Expectations: The Need for LTC Insurance

According to the latest available data, the US population pyramid reflects the aging trend that has been unfolding over the past few decades. The baby boomer generation, born between 1946 and 1964, constitutes a significant portion of the population, resulting in a bulge in the older age groups of the pyramid. Meanwhile, the younger age cohorts, particularly those under 40, form a relatively smaller proportion, indicating declining birth rates in recent years. Additionally, factors such as increased life expectancy and advancements in health care have contributed to a larger population of older adults.

Looking ahead to the next 10 to 20 years, several demographic trends are expected to shape the evolution of the pyramid. One of the most notable trends is the continued aging of the population, driven primarily by the aging of the baby boomer cohort. As this large cohort progresses into retirement age, the older age groups of the population pyramid will expand further, leading to an overall aging of the population. An aging population will increasingly need LTC insurance,[5] and the private market will have to expand to accommodate those needs.

Are Higher Rates Sustainable?

Term premium in the context of Treasury securities refers to the additional yield that investors demand to hold long-term bonds compared to short-term bonds. This premium compensates investors for the risks associated with longer maturities, such as interest rate risk and inflation uncertainty. This premium is affected by economic uncertainty and inflation expectations, Federal Reserve policy and the supply and demand dynamics of long-term government debt issuance.

For retirees, this means potentially higher costs for securing guaranteed income, adjustments in investment strategies and implications for pension plan funding. While higher yields can offer better returns for new investments, the overall impact tends to increase the cost of retirement, especially for those heavily invested in fixed-income assets.

The cost of LTC insurance is closely tied to long-term interest rates. As interest rates rise,[6] insurance premiums may decrease due to higher investment returns for insurers and lower present value of future liabilities. Conversely, if interest rates remain low, insurers may need to charge higher premiums to maintain financial stability and cover future claims.

Benefits of Cash Flow Hedge Accounting to Draw in Insurance Companies

Forward starting swaps on longer maturity issuances can be used to hedge the risk associated with LTC insurance.[7] A forward starting swap is a swap contract that begins at a future date rather than immediately. This allows the parties involved to lock in a fixed rate for a specific period of time in the future, which can help to mitigate the risk of interest rate fluctuations. In the context of LTC insurance, forward starting swaps on longer maturity issuances can be used to hedge the risk of interest rate changes that may affect the cost of providing long-term care over an extended period of time. The key advantage is that the swap has a delayed start date, matching the timing of when the insurer expects to receive premiums and pay claims on the long-term care policies.

The notional amount of the swap is sized to match the expected future liability cash flows from the LTC policies. This allows the insurer to convert its floating rate investment income into a fixed rate, reducing interest rate risk and earnings volatility. The forward starting swap can also potentially receive favorable accounting treatment under the US General Accepted Accounting Principles (GAAP), helping to minimize the impact on the insurer's financial statements. Overall, forward starting interest rate swaps provide an effective way for LTC insurers to manage their interest rate risk exposure and stabilize their financial results over the long duration of these insurance liabilities.

A cash flow hedge is a hedge of the exposure to variability in cash flows that is attributable to a particular risk associated with a recognized asset or liability, or a highly probable forecast transaction. For example, if you have a variable-rate loan, you may use a cash flow hedge to fix the interest payments for a certain period. It defers the effective portion of the changes in fair value of the hedging instrument in other comprehensive income and reclassifies it to profit or loss when the hedged transaction affects income. This means the hedge is effective in stabilizing the cash flows, but it also creates volatility in the equity.

The role of the private sector is crucial in this respect. It can help mobilize premiums and design a mix of long-term Treasury assets and medium-term credit assets to fund this deficit. Chen showed various ways to fund long-term care needs, including the out-of-pocket costs and private LTC insurance in the private sector and the social insurance, Medicaid benefits and other sources in the public sector.[8] Private LTC insurance comprises both standalone and combination policies offered by life insurance companies, which are purchased by middle-aged consumers and may be used to fund the growing budget deficit.

Conclusion

The need for LTC insurance in the coming years can be met if life insurance companies jump-start issuance of such policies. At higher interest rates, such policies look extremely attractive for policyholders as well as issuers. If interest rates were to remain high or move even higher, the attractiveness of the product would only increase. A steady increase of interest rates will bring in new players guided by profitability and ease of risk mitigation by investing in longer-term bonds. An increase in interest rates thus is not to be feared but to be looked on as a new opportunity for an old form of insurance business.

This article is provided for informational and educational purposes only. Neither the Society of Actuaries nor the respective authors’ employers make any endorsement, representation or guarantee with regard to any content, and disclaim any liability in connection with the use or misuse of any information provided herein. This article should not be construed as professional or financial advice. Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Arnab Sarkar is a senior vice president/derivatives trader: fixed income and equity at AllianceBernstein LP. Arnab can be reached at arnab.sarkar@abglobal.com.

Endnotes

- U.S. Long Term Care Market (2025–2030), Grand View Research, n.d., https://www.grandviewresearch.com/industry-analysis/us-long-term-care-ltc-market.

- Richard Rubin, “Tax Cuts Are Here to Stay—and So Are Exploding Budget Deficits,” The Wall Street Journal, September 13, 2023, https://www.wsj.com/politics/tax-cuts-budget-deficits-republicans-democrats-4f2a0d33.

- Eric Wallerstein, “A $1 Trillion Conundrum: The U.S. Government’s Mounting Debt Bill,” The Wall Street Journal, February 16, 2024, https://www.wsj.com/finance/the-u-s-government-will-soon-spend-more-on-interest-payments-than-defense-ee6fbeec.

- Congressional Budget Office, “The Long-Term Budget Outlook: 2024 to 2056,” CBO, February 2026, https://www.cbo.gov/publication/62044 .

- Glenn Ruffenach, “The Odds on Needing Long-Term Care,” The Wall Street Journal, June 6, 2019, https://www.wsj.com/articles/the-odds-on-needing-long-term-care-11559836590.

- Nick Timiraos, “Even if the Fed Cuts Rates, the Days of Ultralow Rates Are Over,” The Wall Street Journal, April 28, 2024, https://www.wsj.com/articles/the-odds-on-needing-long-term-care-11559836590.

- Julia Kagan, “Long-Term Care (LTC) Insurance: Definition, Costs, Alternatives,” Investopedia, July 30, 2023, https://www.investopedia.com/terms/l/ltcinsurance.asp.

-

Yung-Ping Chen, “Funding Long-term Care in the United States: The Role of Private Insurance,” The Geneva Papers on Risk and Insurance 26, no. 4 (2021): 656–66, https://www.jstor.org/stable/41952605.